RBI Cuts Repo Rate to 6%, Projects 6.5% GDP Growth for FY 2025-26

Introduction

The Monetary Policy Committee (MPC), in its 54th meeting and the first of the financial year 2025–26, unanimously decided to reduce the policy repo rate by 25 basis points, bringing it down to 6 per cent with immediate effect. The repo rate is the rate at which the Reserve Bank of India (RBI) lends money to commercial banks, and a cut in this rate is aimed at boosting lending and investment. This decision comes at a time when global economic conditions are becoming increasingly uncertain. Trade tensions have resurfaced, leading to a decline in crude oil prices, weakening of the US dollar, softening bond yields, and corrections in equity markets. While central banks across the world are adjusting their policies to address domestic concerns, they are doing so cautiously.

Within India, the outlook has shown signs of improvement. Inflation, particularly food inflation, has declined more than expected, offering some relief, though global and weather-related risks remain. Growth is recovering after a weak first half in the previous financial year, but it still falls short of the country’s potential. The Monetary Policy Report of April 2025, released alongside the MPC resolution, also outlines the GDP growth forecast and inflation projection for the coming months. This year also marks a milestone for the RBI as it completes 90 years since its establishment on 1st April 1935. Over the decades, it has evolved into a full-service central bank, balancing its roles of managing inflation, supporting growth, and ensuring financial stability.

Key Policy Decisions

- The Monetary Policy Committee (MPC) unanimously decided to reduce the policy repo rate by 25 basis points, bringing it down to 6 per cent with immediate effect. The repo rate is the rate at which the Reserve Bank of India (RBI) lends money to commercial banks.

- As a result, the Standing Deposit Facility (SDF) rate under the Liquidity Adjustment Facility (LAF) has been adjusted to 5.75 per cent. The SDF allows banks to park excess funds with the RBI without any collateral.

- The Marginal Standing Facility (MSF) rate and the Bank Rate have both been revised to 6.25 per cent. MSF stands for Marginal Standing Facility, a provision made by the RBI that enables scheduled commercial banks to obtain overnight liquidity if inter-bank funds completely dry up. It is an emergency facility that allows banks to borrow at a rate higher than the repo rate.

- These rate adjustments are consistent with the RBI’s objective of achieving the Consumer Price Index (CPI) inflation target of 4 per cent, within a flexible band of ±2 per cent, while also supporting economic growth.

Growth Assessment

The Reserve Bank of India has projected real GDP growth at 6.5 per cent for 2025–26, maintaining the same rate as estimated for 2024–25, following a strong expansion of 9.2 per cent in the preceding year. The quarterly projections stand at 6.5 per cent in Q1, 6.7 per cent in Q2, 6.6 per cent in Q3, and 6.3 per cent in Q4. This marks a downward revision of 20 basis points from the February estimate, reflecting heightened global volatility. Agriculture remains on a positive footing, supported by healthy reservoir levels and robust crop production, which is expected to sustain rural demand. Manufacturing is showing early signs of revival amid improved business sentiment, and the services sector continues to demonstrate resilience.

On the investment side, activity is gaining pace on the back of higher capacity utilisation, continued government focus on infrastructure, and strong balance sheets of banks and corporates. Easing financial conditions have also aided this recovery. While services exports are likely to remain steady, merchandise exports could face headwinds from global uncertainties and trade disruptions. Looking ahead, the RBI has projected real GDP growth at 6.7 per cent for 2026–27, suggesting continued recovery momentum.

Inflation Outlook

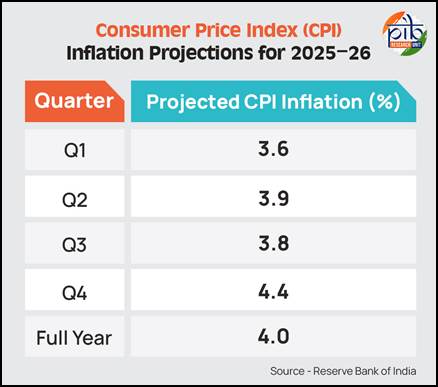

Headline inflation eased during January and February 2025, driven by a sharp decline in food prices. With uncertainties around the rabi crop largely resolved, and second advance estimates indicating record wheat output and higher pulse production than last year, food inflation is expected to soften further. This favourable trend is supported by robust kharif arrivals and a sharp fall in inflation expectations over the next three and twelve months, as reflected in recent surveys. The decline in crude oil prices has further strengthened the disinflationary outlook. Accordingly, Consumer Price Index (CPI) inflation for 2025–26 is projected at 4.0 per cent, with quarterly estimates at 3.6 per cent in Q1, 3.9 per cent in Q2, 3.8 per cent in Q3, and 4.4 per cent in Q4.

While the inflation outlook appears stable, global uncertainties and the possibility of weather-related supply shocks continue to pose upside risks to the inflation path. The Reserve Bank of India has assumed a normal monsoon in framing its projections, and it considers the risks to be evenly balanced at this stage.

External Sector Snapshot

- Robust Services and Remittances: Services exports remained strong in January–February 2025, led by software, business, and transportation services. Net services and remittance receipts are expected to remain in large surplus, cushioning the merchandise trade deficit.

- Sustainable Current Account Deficit: The current account deficit (CAD) for both 2024–25 and 2025–26 is projected to stay well within sustainable levels, supported by resilient external inflows.

- Mixed Investment Flows: While gross FDI remained strong due to stable macroeconomic fundamentals, net FDI moderated because of higher repatriations and outward investments. Net FPI inflows touched USD 1.7 billion in 2024–25, driven by debt inflows despite equity outflows.

- Healthy Forex Reserves: As of April 4, 2025, India’s foreign exchange reserves stood at USD 676.3 billion, offering an import cover of nearly 11 months and reflecting the strength of the external sector.

Liquidity and Financial Market Conditions

- Liquidity Shortage and RBI Intervention: In January 2025, the banking system faced a shortage of funds, known as a liquidity deficit. To address this, the Reserve Bank of India (RBI) provided up to ₹3.1 lakh crore on 23rd January through the Liquidity Adjustment Facility (LAF) – a tool that allows banks to borrow money from the RBI for short periods to manage temporary mismatches in cash flow.

- Improved Liquidity Position: The RBI later infused about ₹6.9 lakh crore into the system, and increased government spending in late March helped further. These actions improved the situation, and by 7th April 2025, the system had a liquidity surplus of ₹1.5 lakh crore – meaning there was more money available in banks for lending and investment.

- Softening of Market Rates: With more liquidity available, the Weighted Average Call Rate (WACR) – the average interest rate at which banks lend to each other overnight – declined and hovered close to the repo rate, which is the interest rate at which the RBI lends money to commercial banks. This indicates stable short-term borrowing costs.

- Lower Funding Costs in Debt Market: The difference between interest rates on Commercial Papers (CPs) and Certificates of Deposit (CDs) – short-term borrowing instruments used by companies and banks – and the 91-day Treasury Bill – a short-term government security – reduced. This narrowing of spreads means that borrowing became cheaper in financial markets. The RBI has stated it will continue to monitor these conditions and take action as needed to maintain sufficient liquidity.

Conclusion

The Monetary Policy Report of April 2025, released alongside the 54th meeting of the Monetary Policy Committee, reflects a balanced approach by the Reserve Bank of India (RBI) to support growth while maintaining price stability. The decision to cut the policy repo rate by 25 basis points to 6 per cent is underpinned by easing inflation, particularly in food prices, and a gradual recovery in economic activity. With GDP growth for 2025–26 projected at 6.5 per cent and inflation expected to remain within the 4 per cent target band, the report signals cautious optimism despite global uncertainties.

On the external front, robust services exports and strong remittance inflows have helped cushion the merchandise trade deficit, keeping the current account deficit at sustainable levels. Meanwhile, improved system liquidity, lower short-term borrowing costs, and stable foreign exchange reserves underscore the resilience of India’s financial system. The RBI has affirmed its commitment to closely monitor evolving conditions and take timely, calibrated measures to preserve macroeconomic and financial stability.

Reaction to the RBI policy | Colliers | Vestian | India Sotheby’s International Realty| Square Yards | Urban Money

Consecutive reduction in benchmark lending rates will boost homebuyers’ sentiments and resultantly improve housing demand particularly in affordable and middle-income segments. Real estate developers across segments also stand to benefit from likely lowering of financing costs. Overall demand and real estate growth is likely to be on the upswing, given the anticipation of further easing in monetary policy. However, global headwinds and trade frictions will remain a key monitorable for all economic sectors including real estate.

RBI has also proposed securitization of stressed assets through a market-based mechanism, in addition to the Asset Restructuring Company (ARC) route. Reduction in borrowing costs coupled with alternate resolution mechanism for stressed assets is likely to benefit real estate stakeholders in the near-mid-term. This is expected to provide significant relief to cash strapped developers and several stalled projects due to financial constraints.

Perspective by Mr. Nitin Bavisi, CFO, Ajmera Realty & Infra India Ltd on the RBI monetary policy

“The RBI has reduced the repo rate by 25 bps and at 6% now indeed delivered on the relief front, and the central bank is ahead of the curve with its policy measures to combat the uncertainties post due to global tariff war.

The central bank has provided relief on the rate front for the second consecutive time. The rate cut is complemented well by the change in policy stance from neutral to accommodative. The change in stance indicates the readiness of the central bank to act as per the prevailing situation. Other than the rate cut and policy stance change, the commentary on inflation indicating further softening of inflation due to better crop production and above normal monsoon expectations.

The RBI has now cut rates by 50 bps in the current calendar year, a move which is expected to further boost demand for real estate.

Lower interest rates are anticipated to propagate better home loan affordability, eventually accelerating housing demand in varied ticket segments.

The other measures like RBI allowing securitisation of stressed assets and co-lending between regulated entities and beyond priority sector, along with ample system liquidity will help boost the credit growth in the system. Barring the tariff war, geopolitical tensions, most economic indicators are positive, including inflation, GDP growth and a normal monsoon year.”

Debopam’s-Chief Economist, Piramal Group quote on the RBI MPC:

There was an opportunity to front end the rate cuts with a 50 bps decline in April’25 since currency has strengthened, inflation fallen below target and US and Indian yield differential rising once again. However, the change in stance and sharp rise in surplus systemic liquidity will do for now. With an accommodative stance, markets now are certain than the only way forward for rates is downwards. Transmission will also improve supported by the liquidity and the fact that share of EBLR loans have now increased to more than 60%, prompting faster pass through of repo declines to end user loan rates.