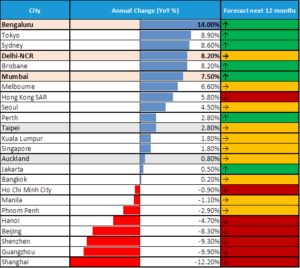

Mumbai, April 18, 2026: Knight Frank, a leading international property consultancy, in its latest report, ‘Asia Pacific Research, Office Markets – Q1 2026’, noted that Bengaluru recorded the highest year-on-year (YoY) growth in prime office rents across the Asia Pacific region recording a rise of 14% in Q1 2026 over same time last year. The performance highlights India’s resilience within the APAC office markets, with rental growth remaining firm across major office markets posting YOY prime office rent growth. Mumbai and Delhi – NCR recorded rent growth of 7.5% and 8.2% YoY respectively during the same quarter.

Out of the 24 prime markets tracked across Asia-Pacific, 18 recorded increased rents sustaining the recovery momentum in Q1 2026, with regional rents rising 0.8% quarter-on-quarter (QoQ), even as the escalation of the conflict in the Middle East reintroduced geopolitical uncertainty. According to the report, sustained demand from India and Australia drove the headline gain, while 18 of 24 monitored cities recorded stable or improving rents, up from 17 in Q4 2025.

Occupancy Cost: Delhi NCR becomes the 6th most expensive prime office rental market in APAC

Across APAC, Hong Kong SAR recorded the highest occupancy cost at USD 158.96 per sq ft per annum, while within India, the prime office market of Delhi-NCR continues to see rental values maintain levels seen in the past four quarters. The prime office rent of the city was recorded at USD 72.33/sqft/year, making it the 6th most expensive office market in the APAC region.

Followed by this, the prime office rent of Mumbai was recorded at INR USD 68.51/sqft/year and was the 8th most expensive commercial market in the APAC region. Further to this, Bengaluru stands 19th with the prime office rent recorded at USD 36.84/sqft/year.

Leasing Activity in Indian Office Market

Leasing demand remained robust with 18.8 mn sf transacted across India’s largest office markets of Bengaluru, Mumbai and Delhi-NCR during the quarter, up 3% from the same period in 2025. Mumbai stood out with leasing volumes reaching a quarterly record of 5.6 mn sf transacted. Unlike previous years, when demand was heavily concentrated in Bengaluru, leasing activity was broad-based across markets, pointing to a more balanced and geographically diversified expansion in office demand. While GCCs remained the primary driver, demand from domestic-focused businesses also noticeably accelerated.

Office completions continue to trail demand, as developer focus remains skewed toward residential projects. The 8.5 million sf delivered during the quarter is less than half of the leases transacted during the quarter. Leasing activity remained overwhelmingly concentrated in prime office assets, a trend which has deepened in recent years, underpinned by the expansion of GCCs and growing integration of flexible workspace solutions within core office portfolios.

Bengaluru led with 14% rental growth (highest in APAC) and 41% of GCC leasing, supported by stable vacancy at 11.8% and a slight landlord bias. Mumbai was the standout performer, recording a peak leasing volume of 5.6 million sq ft and 7.5% rental growth; with vacancy at 16.2%, rents are expected to rise further from INR 4,025 psf per annum. Delhi-NCR saw steady momentum, with rents up 8.2% year-on-year and 3.7% quarter-on-quarter; vacancy at 14.2% is expected to keep rents stable at INR 4,428 psf per annum, reflecting a slight tenant preference.

Shishir Baijal, International Partner, Chairman and Managing Director, Knight Frank India, said, “Leasing demand across India’s prime office markets has remained resilient, with activity becoming more broad-based across Bengaluru, Mumbai and Delhi-NCR. The diversification of demand beyond traditional hubs reflects a maturing office market supported by both global and domestic occupiers. While GCCs continue to anchor demand, the increasing participation of domestic-focused businesses is a notable trend. With supply additions trailing leasing activity and occupiers continuing to prioritise high-quality assets, we expect rental values in prime office markets to remain firm. The structural shift towards premium, future-ready workspaces, along with the growing role of flexible office solutions, will continue to shape the trajectory of India’s office market in the near to medium term.”

APAC Prime Office Rent growth – Q1 2026-

Source: Knight Frank

Tim Armstrong, Global Head of Occupier Strategy and Solutions at Knight Frank, noted that the structural case for prime office space is increasingly difficult for occupiers to sidestep. He added, “While the escalation of the conflict in the Middle East has reintroduced a layer of geopolitical uncertainty, occupier sentiment across Asia-Pacific has remained broadly resilient. Although some occupiers may exercise near-term caution by delaying real estate decisions, this approach is unlikely to be widely feasible as development pipelines will get increasingly constrained across most markets. Occupiers are prioritising quality, future-ready offices that support talent attraction, resilience and long-term operational flexibility.”

He added that the conflict’s impact on energy costs reinforces, rather than undermines, the flight-to-quality thesis. “The sustained impact on energy costs due to the conflict further strengthens the case for well-located, energy-efficient offices with strong access to transport nodes. In an uncertain environment, real estate is increasingly viewed as a strategic enabler of business stability and long-term growth, rather than a discretionary cost.”